RDR, VROL, VCR and VRAD: card dispute life cycle

This article will be primarily focused on the unhappy path of card processing: disputes. I’ll cover the basics and more in-depth structure of dispute processing and resolution. The ultimate goal of this article is for you to better understand the moving pieces of any dispute to be better suited in preventing them or winning the ones that happen.

Quick disclaimer before I continue: most of my articles are Visa-heavy for a very simple reason. I like their docs and visuals and I won’t be spending my breath covering all 4 card networks in-depth unless absolutely necessary.

Dispute is an action taken by a payor (cardholder) to challenge the transaction on their card statement with their issuing bank.

Many people confuse chargebacks with disputes. Dispute ≠ Chargeback. Chargeback is simply a dispute that results in a reversal of a specific transaction that was disputed by the payor.

Dispute Flows: RDR, VROL, VCR and VRAD.

Visa operates all of its transaction disputes through VROL - Visa Resolve Online. Think of VROL as one big database of all transactions processed by Visa where visa can find information on specific transaction that is being disputed. All the dispute flows run within the VROL system.

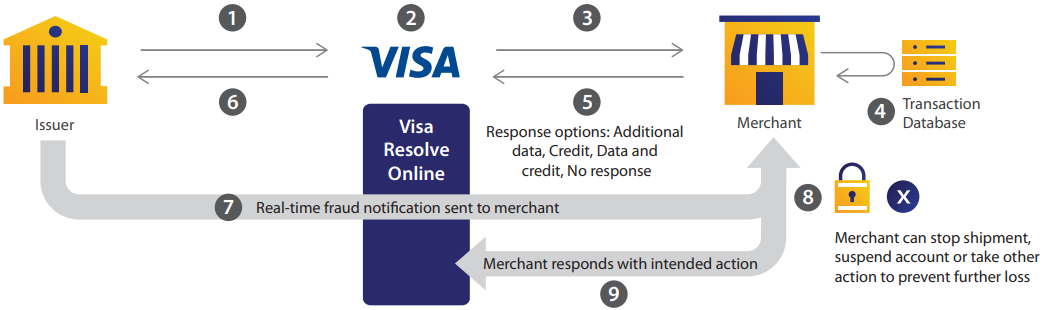

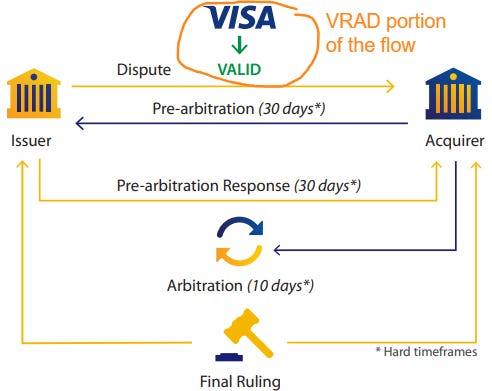

Visa card transaction disputes look roughly like this within VROL:

Fig. 1 From Visa public documentation on VCR, page 3.

Fig. 1 From Visa public documentation on VCR, page 3.Although the graphic lists a Merchant, in reality the communication is through the Acquirer (like Moov) and most Merchants aren’t interacting directly with Visa or any other card networks.

As I’ve mentioned earlier, I work for Moov so I’ll be using Moov’s amazing docs to fill some gaps here.

Issuer identifies transaction that is being disputed within VROL and requests more information by sending a request to Visa.

Visa confirms merchant participation in Visa Merchant Purchase Inquiry solution (VMPI) - a solution that allows merchants to communicate to issuing banks through Visa without necessarily turning transaction into a chargeback. The chargeback can be avoided by cooperating on this step.

Visa sends a request to the acquirer for additional data and acquirer sends it to the merchant. Merchant will be receiving these notifications through webhooks provided by the acquirer.

Merchant and acquirer run internal rules to determine the best response. Essentially they look internally on how valid the dispute is, the size of the dispute, account history, supporting evidence they have on hand etc. and decide on one of the responses listed below. Most of this is done automatically.

Merchant sends one of the following responses:

Respond with additional data. This will be filed through the processor using one of the API end-points or the dashboard; Provide transaction-specific data such as a description of goods purchased or device used.

Respond with customer credit – accept fault and issue a refund to the cardholder.

Respond with additional data and partial credit.

All this can be automated through RDR - skip to section “RDR” to learn more about that flow and its effects.

The response is forwarded to the issuer who can assist cardholder in recognition of the transaction. The cardholder’s bank explains what is the outcome of the dispute and funds settle over the period of 5-7 days.

This is a pretty standard flow. However, Visa came out with VCR - Visa Claims Resolution in 2017 to streamline card dispute resolutions that modify this flow to speed up certain actions. VCR has the ability to modify the flow above and introduce elements of automation.

VCR is a ruleset and a routing system that decides which system will be utilized for each disputed transaction. The routing depends on multitude of factors such as dispute code assigned, transaction amount, time passed after the transaction was processed, eligibility for VRAD and RDR (based on merchant’s enrollment in RDR) etc.

RDR: Rapid Dispute Resolution.

RDR is the first automation to kick in during a dispute process. In simple terms, it can help prevent the formal dispute from occurring by allowing merchants to create rules that automatically cede the dispute to the cardholder.

For example a rule created by the merchant can look like: if a transaction being disputed is below $100, automatically credit the funds to the cardholder.

Key benefit of RDR for a merchant: if a dispute is resolved through RDR, it will not be counted towards the merchants dispute ratio calculation - you can have 50% dispute rate but as long as they are all resolved through RDR, you will be a (almost) perfectly fine merchant to be onboarded by any acquirer. Magic at a cost of losing slightly more disputes.

This information can be found in Visa documentation on RDR here (2nd page is quite relevant to everyone dealing with card acquisition, I recommend actually glancing at it).

RDR Structure.

RDR is operated by verifi - Visa-owned company so think of it as Visa for simplicity.

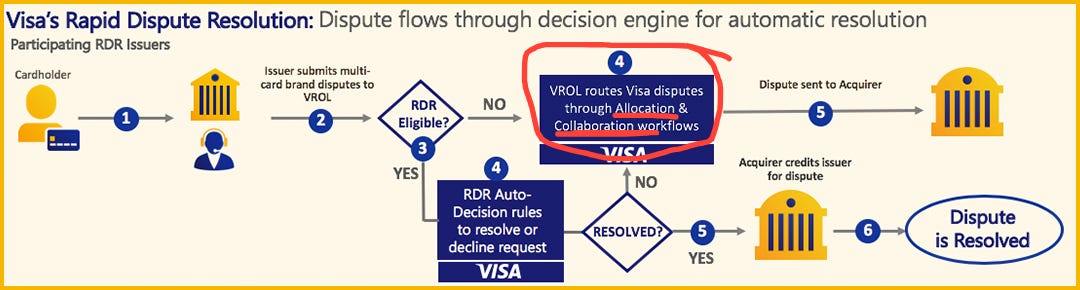

Fig 2. From Visa documentation. Highlighted in red is the reference to the two flows described later: Allocation and Collaboration.

Fig 2. From Visa documentation. Highlighted in red is the reference to the two flows described later: Allocation and Collaboration.RDR works in a very straightforward manner: merchant sets the rules through Verifi that allow for automatic resolution of any disputes before those disputes become chargebacks.

Example: you run Audible - an app that allows you to buy audio books or subscribe monthly to get 1 title per month. You consistently get disputes from customers who forget to unsubscribe after getting a single title. Your monthly subscription is $15 and each dispute costs you $50+ to process.

This is where you setup your RDR (more on this later) and create two rules:

1. Any dispute that is below $16 is auto-refunded through RDR.

2. If the dispute code is 13.2 (where customer claims that they have cancelled a recurring subscription but were still charged) and customer disputed transaction within 30 days, auto-refund through RDR.

If either of these two rules is met, the dispute will be automatically won by the cardholder and they will be refunded through RDR. You save money and energy on disputes, make your customers more satisfied and reduce your chargeback ratio. Win-win.

I have mentioned earlier that RDR-resolved disputes don’t go on the merchant’s record as a chargeback. However, to provide additional visibility for the acquirers, RDR will still end up on the merchant’s record in VROL in the following format: mnn.c.c-YDDD

where m = Merchant indicator (“M”)

nn = Dispute Category

c.c = Dispute Condition

Y = last digit of the year (2017 and 2007 would both be represented by “7”)

DDD = exact day of the year (ex: 107th day of year 2017).

Setting up RDR as a merchant.

Depending on the PSP that you use, they might allow you to setup RDR directly through their system. Companies like Nuvei and Stripe offer such capabilities. If they do - go ahead and set it up directly there.

If your PSP doesn’t offer such capabilities (for example, Moov supports RDR use but doesn’t allow its setup directly through the dashboard), you will have to go through Verifi.

I have called and emailed them four times in the span of two weeks. No instructions were sent to me. If you want to enroll into RDR, I will be happy to help you directly: it is easier to move things along when it’s Moov’s customer (I’m assuming you’ll work with us) wants to enable RDR, opposed to “I’m writing an article on this…” Set us some time to talk here if you’re interested.

Dispute code assignment.

If a transaction is not RDR-eligible, we move to the next step: further routing of a dispute using the VCR’s rules. See the part highlighted in red in Fig. 2.

This process starts with the dispute code assignment to a transaction.

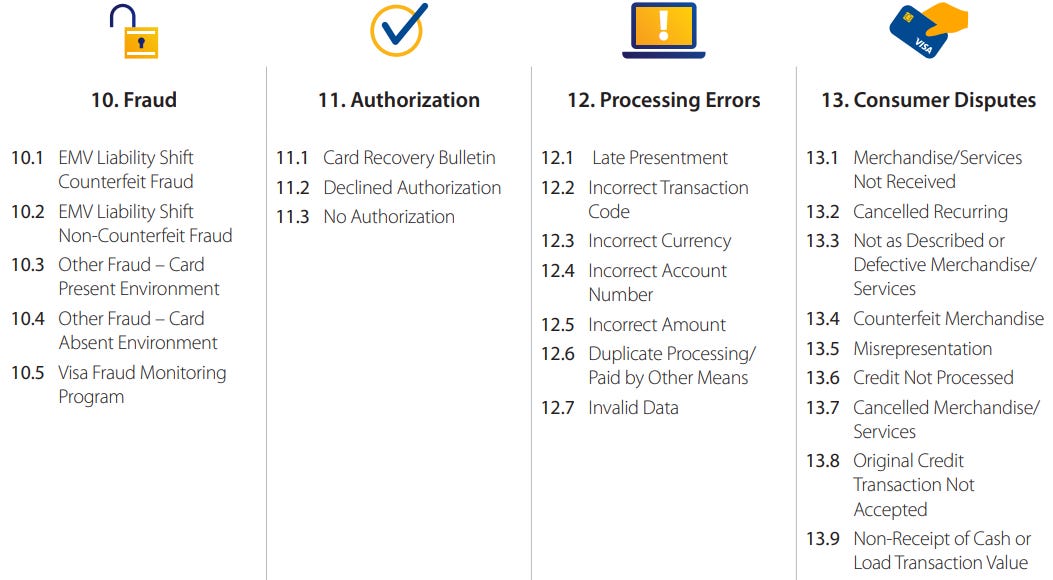

According to Visa’s dispute management guide, page 8, has four dispute categories (things that cause disputes):

10.x code: Fraud (Category 1 - Allocation)

11.x code: Authorization (Category 1 - Allocation)

12.x code: Processing Errors (Category 2 - Collaboration)

13.x code: Consumer Disputes (Category 2 - Collaboration)

Here is the list of all the united codes that rule which dispute code will be assigned to which transaction according to the VCR rules within the VROL flow.

The codes are assigned by the Issuer based on the information contained in their system and reasoning provided by their client (cardholder who originated the dispute). VROL in this case acts as a source of truth for VCR rule-set that establishes if the transaction is actually eligible for the code assigned by the issuer.

IF VCR rules that the transaction is ineligible for the code assigned, the dispute will be auto-rejected without ever getting to the acquirer and will have to be re-submitted. There is no arbitration for such decisions.

Example: cardholder initiates a dispute for transaction and claims that a certain transaction was fraudulent. Their bank (issuer) starts a dispute process within VROL and assigns it a 10.x code.

VROL sees that the transaction was 3DS secure (meaning that the cardholder verified their identity during a purchase through a password or biometric). This automatically means that the transaction wasn’t fraudulent so VROL rules that the code assigned is wrong and if the issuer wants to dispute the transaction it would need to be filed under a different code.

There is a strong overlap here between VRAD and VCR checks on the code eligibility. The goal for Visa in both systems is to automate the decisions on flawed disputes that are most likely made by unhappy customers. I’ll talk more about VRAD in what follows.

You can view the full table of these codes along with the appropriate resolution requirements here.

Routing based on the dispute code.

Once the code gets assigned, the system (VROL) can alter the flow slightly and introduce appropriate automations that would be assigned following the VCR rules.

Allocation: Fraud and Authorization (Category 1).

For Category 1 (codes 10.x and 11.x), Visa uses VRAD (Visa Risk-based Auto Dispute) to automatically review the disputes submitted by the cardholder and rule automatically on whether or not the dispute is valid.

Example of VRAD use: customer files a dispute for a $54 transaction claiming that it was fraudulent. They purchased a pair of shoes in the store; Visa will see that the payment method was CP (Card Present) and card entry mode was “Chip” (meaning that the customer physically inserted the card into the terminal). They will verify that the Merchant had the terminal capability to read chips (aka verify that it’s not tap-only).

The only logical conclusion is that the customer went to the store, inserted their card with the chip (the MOST secure method of payment) and completed the transaction. It can’t be fraud so Visa denies the request right there and then without it going to the acquiring bank or the merchant.

If VRAD yields a result beyond reasonable doubt (that can’t be disputed by either issuer or merchant) the case is closed. In the image above, the result of VRAD shows “VALID” which means that the case is closed and transaction is determined as fraud with funds returned to the cardholder.

If the result is “not VALID”, we continue to the standard flow.

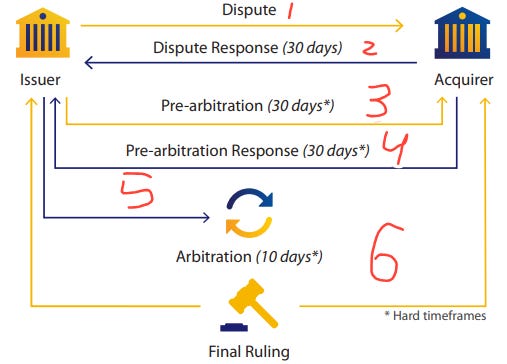

Collaboration: Processing Errors and Consumer Disputes (Category 2).

All disputed transaction with the code 12.x and 13.x are pushed through this flow, unless they are RDR eligible.

As the name implies, this process relies more heavily on collaboration between acquirer and issuer with Visa coming in for arbitration only if all else fails.

Here is a step-by-step breakdown of the dispute routed through Collaboration flow (some steps are shortened since they are identical to the previously covered steps):

Dispute: the cardholder starts a dispute.

Dispute response: Merchant responds with one of the following actions -

Respond with additional data and refuse liability. This will be filed through the processor using one of the API end-points or the dashboard; Provide transaction-specific data such as a description of goods purchased or device used.

Respond with customer credit – accepting the fault and issuing refund to the cardholder.

Respond with additional data and a partial credit.

Pre-arbitration: the issuer initiates a pre-arbitration process if they are not willing to accept the response of the acquirer. For example, if the merchant provided partial refund and data proving that the rest of the transaction is valid, the issuer may dispute that claim and start the pre-arbitration process.

Pre-arbitration response: acquirer and merchant review the argument of the issuer and decide if they want to accept it or not. This is the last line of defense before one of the most expensive parts in the dispute process, humans get involved at this point almost at all times. Acquirer and merchant may issue additional partial credit or fully yield to avoid arbitration.

Arbitration: if the second response still doens’t satisfy the issuer, they will file for arbitration through Visa. Usually this process costs $500+ for acquirer and therefore it very rarely gets to this stage.

During the arbitration, Visa reviews all the information collected in steps 1-4 and makes the decision.Appeal: although it is not listed on the official chart, there is an option to appeal Visa’s arbitration decision as long as the transaction being disputed is greater than 5,000USD. The decision on the appeal is final.

It is important to note that in a Collaboration case, Visa will push the funds to issuer when the dispute is initiated (temporary credit as described earlier) and if the acquirer declines the dispute reasoning (their response in Step 2 is negative), the funds are moved back to acquirer.

The funds will be with the acquirer until liability is decided.

Wrap-up + Call To Action.

This, just like my previous article, took A LOT of time to write: research, the writing process itself and MULTIPLE re-writes. That being said, I strongly suggest that you sign up for AFT publication on Substack.

Resources.

Visa’s dispute management guide that covers the basics of responding to a dispute: https://usa.visa.com/content/dam/VCOM/global/support-legal/documents/merchants-dispute-management-guidelines.pdf

Moov’s documentation of dispute flow: https://docs.moov.io/guides/money-movement/accept-payments/card-acceptance/disputes/#respond-to-disputes

Visa Claims Resolution documentation: https://usa.visa.com/dam/VCOM/download/merchants/visa-claims-resolution-efficient-dispute-processing-for-merchants-VBS-14.APR.16.pdf

Information on RDR provided by verifi: https://www.verifi.com/in-the-news/get-ready-for-rdr.html

VRAD one-pager issued by Visa: https://usa.visa.com/content/dam/VCOM/regional/na/us/Solutions/pps/visa-risk-based-auto-dispute-one-pager.pdf

Visa documentation on 3D Secure: https://corporate.visa.com/en/solutions/visa-protect/insights/3d-secure.html

Visa documentation on Rapid Dispute Resolution process: https://usa.visa.com/dam/VCOM/global/support-legal/documents/proper-identification-of-rdr-transactions-and-service-activation.pdf

Additional information on the collaboration dispute flow: https://academy.pega.com/topic/collaboration-visa-disputes/v1

AFT: instant debit pulls through Account Funding Transactions.